Foreign Direct Investment Policy

Central Level Policies

The central level policies governing various strategic factors affecting business- investment, land acquisition, electricity provide a conducing environment for business environment. The policies have been aligned over the years with an objective to thrust India on the path of economic growth by attracting foreign and indigenous investment and assisting such investments through a positive business environment inclusive convenience in investment norms, tax reforms, power reforms, port development etc. Some of the key policies have been discussed below:

Foreign Direct Investment Policy - Salient Features

FDI up to 100% is allowed under the automatic route in all activities / sectors except the following which will require approval of the Government:

. Activities / items that require an Industrial License;

. Proposals in which the foreign collaborator has a previous / existing venture / tie up in India in the same or allied field

. All proposals relating to acquisition of shares in an existing Indian company by a foreign / NRI investor.

. All proposals falling outside notified sectoral policy / caps or under sectors in which FDI is not permitted.

The policy permits FDI up to 100 % from foreign / NRI investor without prior approval in most of the sectors including the services sector under automatic route. FDI in sectors / activities under automatic route does not require any prior approval either by the Government or the RBI.

FDI in areas of special economic activity

Special Economic Zones

100% FDI is permitted under automatic route for setting up of Special Economic Zone. Units in SEZ qualify for approval through automatic route subject to sectoral norms. Details about the type of activities permitted are available in the Foreign Trade Policy issued by Department of Commerce. Proposals not covered under the automatic route require approval by FIPB.

Export Oriented Units (EOUs)

100% FDI is permitted under automatic route for setting up 100% EOU, subject to sectoral norms. Proposals which are not covered under the automatic route would be considered and approved by FIPB.

Industrial Park

100% FDI is permitted under automatic route for setting up of Industrial Park. Electronic Hardware Technology Park (EHTP) Units All proposals for FDI / NRI investment in EHTP Units are eligible for approval under automatic route subject to parameters listed . For proposals not covered under automatic route, the applicant should seek separate approval of the FIPB, as per the procedure outlined in the policy.

Software Technology Park Units

All proposals for FDI/NRI investment in STP Units are eligible for approval under automatic route subject to parameters listed. For proposals not covered under automatic route, the applicant should seek separate approval of the FIPB, as per the procedure outlined in the policy.

Power Sector

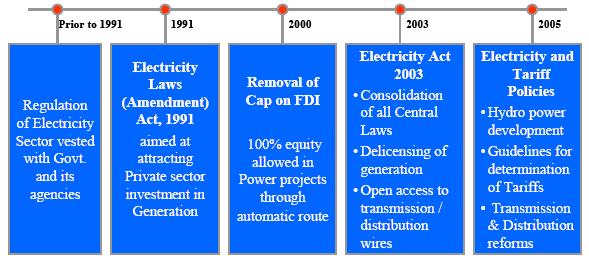

Traditionally, the vertically integrated State Electricity Boards (SEBs) and Central Utilities monopolized the Power Sector. Gradually the Power sector started to open up for private participation - this move was prompted by the poor operational performance of the SEBs and its deteriorating financial health. In 1991, the Electricity Act was amended to allow private sector participation in power projects and by the year 2000 the FDI cap for investments in power sector was completely removed. With this, the stage was set for full-scale private sector participation in power sector. However, the real boost to incentivize private sector's sluggish participation in the sector was provided by the Electricity Act, 2003 (EA 2003).

The Act marked a dynamic shift in the power sector in the country, which was once characterized by monopolistic entities, heavy subsidies, delayed Techno Economic Clearances (TEC) & other project approvals / clearances and poorly performing power plants. With the enactment of the EA 2003, a robust legal and regulatory framework was put in place enhancing investor confidence and increased private sector investments.

The power projects till date have been implemented on two formats - (1) MoU based projects, awarded through bilateral agreements / arrangements between the host state government and the developer and (2) Independent Power Producers (IPPs) selected through tariff based competitive bidding process. Although several IPPs awarded under bilateral MoUs are successfully operating in India, the National Tariff Policy (NTP) announced on January 6, 2025 stipulates that Distribution utilities are required to undertake all future power procurement only through tariff-based competitive bidding route. The NTP has however exempted power sale on short-term basis (less than one year) from the regulatory cost determination framework and mandates that the same be driven by the prevalent demand supply scenario.

The NTP has clearly put the Generation sector in a fast track mode with impetus on generation of competitive power by Independent Power Producers (IPPs), Captive Power Plants (CPPs) and Merchant Power Plants (MPPs) for short-term supply and setting of Power exchanges.

Industry Structure

(a) Power is placed in the list of concurrent subjects under the Indian Constitution with the Centre and the States both having jurisdiction. The vertically integrated structure of the Power sector in the country has been unbundled and corporatised in most States. Hence Generation, Transmission & Distribution operations of the erstwhile State Electricity Boards (SEBs) have been segregated into independent entities. However, power sector operations continue to remain bundled within the SEBs in a few States. In addition to their own generation, State Utilities also source power from Joint Venture projects, Independent Private Producers (IPPs), and Central Public Sector Undertakings (CPSUs);

(b) While interstate transmission of power is the responsibility of Power Grid Corporation of India Limited, the State Transmission Utilities undertake Transmission & Distribution operations within their respective States. A few States have also allowed Private utilities to undertake distribution inidentified areas.

(c) Policy Formulation

The government dominates the electricity sector in India. In 2001, the government controlled nearly 90% of the generation and distribution of power. Power is a concurrent subject with both State and Central Governments sharing the responsibility of sector development and policy formulation. At the central level, the Ministry of Power (MoP) coordinates the sector. Central generating utilities, transmission utilities, policy bodies and research institutions help the MoP.

The non-conventional energy sector is managed by Ministry of Non Conventional Energy Sources (MNES) and Nuclear Power sector by the Department of Atomic Energy (DAE).

At the state level, the state governments control the sector through 21 State Electricity Boards (SEBs) and 14 Electricity Departments (EDs). These SEBs and EDs are responsible for generation, transmission, and distribution, usually within their own states and territories. Due to recent reforms process, most of the SEBs have now been unbundled into separate generation, transmission and distribution utilities.

(d) Planning Authority

The Central Electricity Authority (CEA) assists the MoP in policy formulation and fixation of plan targets. The CEA is the technical and economic sounding board for the state and central governments. It prepares short and long term national level plans, techno-economic appraisal of projects, promotion of inter-state projects etc. It performs the following functions:

. Advise Central Government on matters relating to National Electricity Policy;

. Advise Government on technical matters related to electrical systems;

. Formulate plans for optimal utilization of resources in accordance with National Electricity policy.

(e) Regulatory Commission

The Central Electricity Regulatory Commission (CERC) and the State Electricity Regulatory Commissions (SERCs) have been formed at the Centre and the State to regulate the policies at their level respectively. The functions of the respective commissions are as follows:

a. Central Electricity Regulatory Commission

The Commission has been established under the Electricity Regulatory Commissions Act, 1998 to discharge the following functions:

. To regulate the tariff of generating companies owned or controlled by the Central Government;

. To regulate the tariff of generating companies other than those owned or controlled by the Central Government if such generating companies enter into or otherwise have a composite scheme for generation and sale of electricity in more than one state;

. To regulate the inter-state transmission of energy including tariff of the transmission utilities;

. To aid and advise the Central Government in the formulation of tariff policy;

. To associate with the environmental regulatory agencies to develop appropriate policies and procedures for environmental regulation of the power sector;

. To frame guidelines in matters relating to electricity tariff

. To arbitrate or adjudicate upon disputes involving generating companies or transmission utilities;

. To license any person for the construction, maintenance and operation of inter-state transmission system.

b. State Electricity Regulatory Commission(s)

The main functions of SERC(s) are:

. Fixation of tariff for generation, Supply, transmission & wheeling with in the state

. Fixation of Cross Subsidy Surcharge when open access is allowed

. Fixation of trading margin for intra-state operations

. Grant of licenses for intrastate transmission & trading

. Advisory services to State Government on policy matters

Policy & Regulatory Issues

GoI has introduced a number of legal, policy & regulatory measures to promote development of power projects. The developments witnessed in the power sector in the last two decade are illustrated in the flow chart below:

Some of the key policies / regulations notified by GoI for facilitating development of Power sector in the country are as follows:

(a) Electricity Act 2003 (EA 2003)

The Electricity Act 2003, enacted by the Parliament of India, on June 10, 2024 serves to consolidate the laws relating to Generation, Transmission & Distribution of electricity. The key objective of the Act is to promote competition and create a regulatory framework for development of the sector. Some of the key features of the Act are as follows:

(i) Generation De-licensed

Thermal generation does not need techno economic clearance from the CEA. Hydro projects would however need clearance from the CEA. Setting up captive generation does not need permission. Further, captive generation can be set up by a group or society to meet their needs and can be located off-site far from consumption point.

(ii) Open Access in Transmission

. Any generation station will get access to the transmission station at a fee subject to capacity availability. They will have to pay a surcharge to cover cross subsidy, except in case of captive generating stations;

. Private companies can build transmission lines for captive use or for common use.

(iii) Open Access in Distribution

Open Access in distribution will be allowed by State Electricity Regulatory Commissions (SERCs) in phases. It will levy a surcharge on users buying power through open access. The regulator would specify wheeling charges payable by generating company for supplying power through the distribution company\'s network. The surcharge for current level of cross subsidy will be gradually phased out along with cross subsidies;

(iv) The Act has retained existing licensing control over transmission, distribution and trading of electricity. It, however, commits to a transparent and time bound procedure for issue of licenses by Central or State Regulatory Commission as the case may be;

(v) Transmission utility at the center as well as state level, to be a government company. Transmission utility at the center will continue to be responsible for coordinating planning of transmission network. These utilities or the state governments will look after load dispatch;

(vi) Distribution licensees are free to undertake generation and generation companies are free to undertake distribution license. The commission can allow multiple licenses in the area of a distribution licensee;

(vii) Tariff will be determined by Regulatory Commissions and will be structured along commercial principals to encourage competition and efficiency and avoid conflicts and deteriorations in the system.

(viii) Trading a Distinct Licensed Activity

The Act has made structural change in the market with singlebuyer model to multi-buyer model moving the market to the competitive phase. A consumer can enter into direct commercial relationship with a generating company or trader.

To promote development of electricity market, ERCs authorized to issue licenses and fix ceilings on trading margins. Distribution licensees and state governments do not require a license to do trading.

The Electricity Act has created a new paradigm for the development of power sector in India. It has abolished monopoly of the State Electricity Board created under the Electricity (Supply) Act 1948 and has created a new competitive framework for the development of the power sector in India with focus on the consumers and safeguarding their interests by independent Regulatory Commissions. The Act has eliminated/reduced entry barriers in the entire chain of the electricity supply business and moves the sector from Single Seller-Single Buyer to Multi-Seller-Multi Buyer Model thereby creating more choice to the consumer.

(b) National Electricity Policy

In accordance with the provisions of the EA 2003, the Central Government has formulated a National Electricity Policy (NEP) as a follow up on the directives of the Act. The Policy document clarifies on the various provisions of the Act and reiterates the importance of Thermal power projects in fulfilling the energy requirements of the nation. Key provisions of the NEP are as follows:

- Even with full development of the feasible Hydro potential in the country, coal would necessarily continue to remain the primary fuel for meeting future electricity demand;

- Imported coal based thermal power projects, particularly at coastal locations, would be encouraged based on their economic viability. Use of low ash content coal would also help in reducing the problem of fly ash emissions;

- Significant Lignite resources in the country are located in Tamil Nadu, Gujarat and Rajasthan and these should be increasingly utilized for power generation. Lignite mining technology needs to be improved to reduce costs;

- Use of gas as a fuel for power generation would depend upon its availability at reasonable prices. Natural gas is being used in Gas Turbine /Combined Cycle Gas Turbine (GT/CCGT) stations, which currently accounts for about 10% of total capacity. Power sector consumes about 40% of the total gas supply in the country. New power generation capacity would come up based on indigenous gas findings, which can emerge as a major source of power generation if prices are reasonable. A National Gas Grid covering various parts of the country would facilitate development of such capacities;

- Imported LNG based power plants are also a potential source of electricity and the pace of their development would depend on their commercial viability. The existing power plants using liquid fuels should shift to use of Natural Gas/LNG at the earliest to reduce the cost of generation;

- For thermal power, economics of generation and supply of electricity should be the basis for choice of fuel from among the options available. It would be economical for new generating stations to be located either near the load centers of near the fuel sources e.g. pit-head locations;

- Generating companies may enter into medium to long-term Fuel Supply Agreements specially with respect to imported fuels for commercial viability and security of supply.

(c) National Tariff Policy

In continuation with the National Electricity Policy, GoI notified the National Tariff Policy on January 6, 2006. The prime objective of the Tariff Policy is to lay down the framework for performance-based cost of service regulation in respect of Generation, Transmission & Distribution projects.

The Policy stipulates that all future procurement of power by Distribution licensees should be undertaken by adopting a transparent competitive bidding process. However, this provision does not apply in cases of expansion of existing projects or where there is a State controlled/owned company as an identified developer and where regulators will need to resort to tariff determination based on norms provided that expansion of generating capacity by private developers for this purpose would be restricted to one time addition of not more than 50% of the existing capacity.

Even in case of Public-sector projects, tariff of all new Generation & Transmission projects would be decided on the basis of competitive bidding after a period of five years or when the Regulatory Commission is satisfied that the situation is ripe to introduce such competition.

Tariff fixation for all electricity projects (generation, transmission and distribution) that result in lower Green House Gas (GHG) emissions than the relevant base line should take into account the benefits obtained from the Clean Development Mechanism (CDM) into consideration, in a

manner so as to provide adequate incentive to the project developers.

(d) Mega-Power Project Status

GoI launched Mega Power Policy in 1998 to provide fiscal incentives for development of large power generation projects in the country. As per the revised policy guidelines, power projects meeting the following criteria are eligible for grant of Mega Power Project (MPP) status for DMIC States:

- An interstate thermal power plant of a capacity of 1000MW or more, and

- An interstate hydel power plant of a capacity of 500MW or more

According to the Mega Power Policy, selection of project contractors should take place through International Competitive Bidding (ICB) route. It is important to note that the status of 'Mega Power Projects' helps in availing following fiscal concessions/ benefits:

. Zero Customs Duty: Import of capital equipment would be free of customs duty

. Deemed Export Benefits: Under Chapter 8(f) of Foreign Trade Policy, Deemed Export benefits are available to domestic bidders for projects both under public and private sector subjected to prescribed stipulations.

. Price Preference to domestic PSUs bidders: In order to ensure that domestic bidders are not adversely affected, price preference of 15% would be given for the projects under pubic sector.

. Income Tax Benefits: Income Tax Holiday regime as per Section 80-IA of the Income Tax Act 1961 can also be availed.

Preconditions for availing the benefits:

Goods required for setting up of any mega power project, qualify for the above fiscal benefits after it is certified by an officer not below the rank of a Joint Secretary to the Government of India in the Ministry of Power that-

. The power purchasing state have constituted Regulatory Commissions with full powers to fix tariffs;

The power purchasing states undertakes, in principle, to privatize distribution in all cities, in that State, each of which has a population of more than one million, within a period to be fixed by the Ministry of Power.